Definition

The financial accounting term general ledger refers to a physical or electronic document that contains a record of the company's financial accounts. Companies can have subsidiary ledgers in addition to their general ledger.

Explanation

In the past, general ledgers were physical books containing the transactions affecting the company's assets, liabilities, owner's equity, revenues and expenses. Today, most large companies use software applications such as Enterprise Resource Planning (ERP) tools to manage and store this information.

Subsidiary ledgers, also known as sub-ledgers, are frequently used to store information at a more granular level. For example, there may be a sub-ledger for accounts receivable or revenues. As part of the accounting cycle, transactions are posted to the general ledger using a double-entry approach; which involves both a debit and credit for each entry.

In practice, a journal is used to record and store transactions prior to posting in a ledger account. When a debit or credit is posted to the ledger, a reference number is recorded alongside, or assigned to, the corresponding journal entry. This process provides the accounting department with a tracking mechanism to ensure all journal entries are eventually posted to the company's general ledger.

The information contained in the general ledger is extracted to produce a trial balance. Once a series of adjustments have been made to these accounts, it's possible to produce the company's financial statements.

Example

On January 15th, 20XX, Company A purchases $500,000 in meters from its supplier Company XYZ, payable in 90 days. The following entry would be made in Company A's journal.

Date | Account Description | Account Number | Debit | Credit |

1/15/20XX | Meters | 380 | 500,000 | |

Accounts Payable | 232 | 500,000 | ||

Purchase of $500,000 in meters from Company XYZ, payable in 90 days. | ||||

The information from Company A's journal is then recorded in the appropriate ledger accounts using the double-entry method.

Date | Account Description | Account Number | Debit | Credit |

1/15/20XX | Meters | 380 | 500,000 | |

Purchase of $500,000 in meters from Company XYZ, payable in 90 days. | ||||

Purchase of $500,000 in meters from Company XYZ, payable in 90 days.

Date | Account Description | Account Number | Debit | Credit |

1/15/20XX | Accounts Payable | 232 | 500,000 | |

Purchase of $500,000 in meters from Company XYZ, payable in 90 days. | ||||

Related Terms

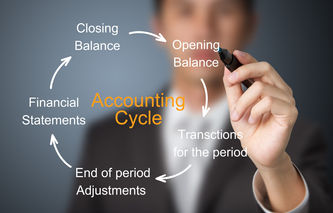

The term accounting cycle refers to the framework and processes followed in each accounting period. The accounting cycle begins with the identification of events and transactions, and ends with the after-close trial balance.

The term accounting cycle refers to the framework and processes followed in each accounting period. The accounting cycle begins with the identification of events and transactions, and ends with the after-close trial balance. Moneyzine EditorDecember 12th, 2023

Moneyzine EditorDecember 12th, 2023 Also referred to as "receivables," this is the accounting term used to describe claims the company has against others for goods, services, or money. Accounts receivable are usually non-written promises to pay for goods or services received but not yet paid for by a customer.Moneyzine EditorJanuary 3rd, 2024

Also referred to as "receivables," this is the accounting term used to describe claims the company has against others for goods, services, or money. Accounts receivable are usually non-written promises to pay for goods or services received but not yet paid for by a customer.Moneyzine EditorJanuary 3rd, 2024 The accounting industry generates billions of dollars. Accounting industry statistics indicate the size of the accounting industry was $544.06 billion in 2020. It gives us an idea of how many accounting events and transactions occur every day in the world.Moneyzine EditorJanuary 16th, 2024

The accounting industry generates billions of dollars. Accounting industry statistics indicate the size of the accounting industry was $544.06 billion in 2020. It gives us an idea of how many accounting events and transactions occur every day in the world.Moneyzine EditorJanuary 16th, 2024 The accounting industry generates billions of dollars. Accounting industry statistics indicate the size of the accounting industry was $544.06 billion in 2020. It gives us an idea of how many accounting events and transactions occur every day in the world. In this article, we will explain what are accounting events and transactions. The term accounting event refers to a change in an item that should be reflected in the company's financial statements. Accounting events can be internal or external and usually involve a change in assets, liabilities, revenues, expenses or owner's equity.Moneyzine EditorDecember 12th, 2023

The accounting industry generates billions of dollars. Accounting industry statistics indicate the size of the accounting industry was $544.06 billion in 2020. It gives us an idea of how many accounting events and transactions occur every day in the world. In this article, we will explain what are accounting events and transactions. The term accounting event refers to a change in an item that should be reflected in the company's financial statements. Accounting events can be internal or external and usually involve a change in assets, liabilities, revenues, expenses or owner's equity.Moneyzine EditorDecember 12th, 2023- The financial accounting term trial balance refers to a listing of all accounts found in the company's general ledger, along with the balance found in each account. Companies conduct both an unadjusted and post-closing trial balance as part of the accounting cycle.Moneyzine EditorSeptember 21st, 2023

- The financial accounting term special journals refers to a series of dedicated documents used by smaller businesses to chronologically record transactions before posting to the general ledger. Typically, these special journals include the following categories: cash receipts, credit sales, purchases on account, and cash payments.Moneyzine EditorSeptember 21st, 2023